How to Stay on Track Financially with Simple Steps and Smart Habits

Busy professionals and young families trying to get serious about personal finance management often hit the same wall: money comes in and goes out, but it never feels clear where it’s headed. Budgeting challenges pile up when spending is inconsistent, bills rotate, and financial goal setting stays vague or gets pushed aside. The confusion gets worse when managing assets and liabilities feels like guesswork, so progress looks smaller than it is. The good news is that financial literacy for beginners is a learnable skill, and clarity creates momentum.

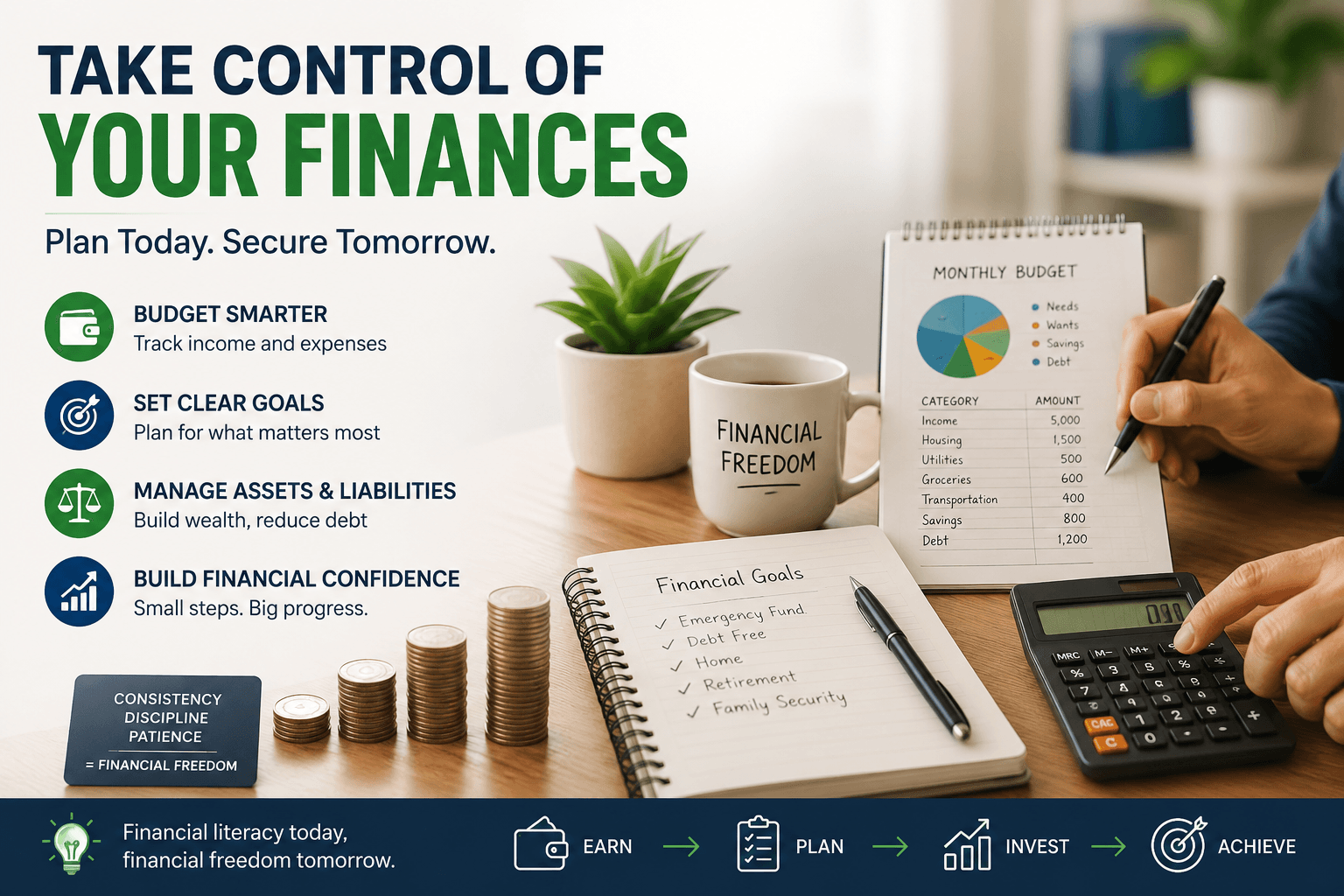

Set Up a Budget System You Can Actually Follow

This quick process helps you see what you own, what you owe, and where your money should go each week. It matters because a simple system beats willpower when life gets busy, and spending gets unpredictable.

- List what you own and what you owe Start with two lists: assets (cash, savings, car value, retirement accounts) and liabilities (credit cards, loans, medical bills). Add current balances and due dates so you can spot the payments that need attention first. This turns “guessing” into a clear starting point you can measure.

- Choose a few budget categories you can stick to Create categories that match real life: housing, groceries, transportation, debt, savings, and a small “fun” line to prevent burnout. Keep it simple, then set a rough limit for each category based on what you typically spend. If you want a shortcut, download helpful tools that give you ready-made templates.

- Track expenses with one method for 14 days Pick one tracking system: an app, a notes list, or a single spreadsheet, then record every purchase for two weeks. Label each expense with your categories so you can see patterns fast, not just totals. The goal is awareness, not perfection.

- Set one money goal and tie it to a weekly action Choose one clear target like “build a $500 buffer” or “pay off one card,” then decide the weekly move that makes it happen (auto-transfer $25, pay $40 extra, cancel one subscription). Treat it like a tiny appointment with your future self. Keep repeating it because median or mean times for habit formation often take weeks, not days.

- Review, adjust, and automate the next paycheck At the end of the two weeks, compare what you planned vs. what you spent and adjust unrealistic category limits. Then automate the most important items first: bills, minimum debt payments, and savings. Automation makes your plan run even when your schedule is packed.

Raise Your Income: Prep for a Better Job in One Hour

Once your budget is realistic and your expenses are under control, increasing your income can make the whole plan easier to stick to. A straightforward way to improve your financial situation is to find a better-paying job, but before you start applying, take an hour to get your resume looking stellar and professional. Using a free online resume template can speed this up significantly: you can pick from a library of professionally designed options, then customize it with your own copy and a look that fits you.

If you want a quick starting point, a resume maker lets you choose a template and add your details, plus photos, colors, and images, so you end up with an application-ready resume without overthinking the design. With your resume refreshed, you’ll be in a stronger position to pursue a new role, and next you’ll lock in progress with a few simple weekly money habits that keep your finances moving forward.

Weekly Money Habits That Keep You Steady

When life gets busy, habits keep your money plan running on autopilot. Pick a few that fit your week, then repeat them until staying on track feels normal.

Weekly Money Check-In

- What it is: Spend 10 minutes to review bank statements and tagging purchases as needs, wants, or bills.

- How often: Weekly

- Why it helps: You spot leaks early and adjust before overspending becomes a pattern.

Automatic “Pay Yourself First” Transfer

- What it is: Set an automatic transfer to savings right after each payday.

- How often: Every payday

- Why it helps: A habit of saving supports stability, even when income changes.

One-Goal Spending Rule

- What it is: Choose one priority for the week and pause nonessential buys.

- How often: Weekly

- Why it helps: Clear priorities reduce impulse spending without feeling restrictive.

Debt “Minimum Plus” Payment

- What it is: Pay the minimum, plus a small extra amount toward one target balance.

- How often: Monthly

- Why it helps: Consistent extra payments speed progress and build confidence.

Emergency Fund Temperature Check

- What it is: Check your emergency savings and pick one action to refill it.

- How often: Monthly

- Why it helps: You stay prepared for surprises without derailing your goals.

Money Tracking and Budgeting Tool FAQs

Q: What’s the simplest way to start budgeting if I feel overwhelmed? A: Start with one category: track all “food” spending for one week and set a gentle cap for the next week. Keep the rest of your money routine the same so you do not burn out. Once that feels steady, add one more category.

Q: How do budgeting apps compare to personal finance software? A: Apps are great for quick check-ins, notifications, and on-the-go spending awareness, and the Mobile Apps segment held a dominant market position, 72.6% share, partly because phones are always nearby. Personal finance software often goes deeper with reports, planning, and account tracking across goals.

Q: What features should I look for in a money-tracking tool? A: Prioritize automatic transaction import, custom categories, and clear monthly summaries. Make sure it can help you track income, expenses, budgets, informed financial decisions without feeling complicated.

Q: Can I stay on track without buying a subscription app? A: Yes. Use a free spreadsheet, your bank’s built-in spending categories, or a simple notes list of totals. If you want guidance, try a free budget calculator to map out a starting plan.

Q: What should I watch for when choosing financial advisory services? A: Ask how they are paid, what services are included, and how often you will review progress. Look for a clear scope, plain-language explanations, and a plan that respects your priorities.

Turn Simple Money Habits Into Long-Term Financial Stability

Staying on track financially is tough when bills, goals, and “one-time” expenses keep pulling attention in different directions. The answer is a steady approach: ongoing budget evaluation, clear priorities, and simple tools that support motivating financial habits instead of adding friction. Applied consistently, this summary of financial best practices helps maintain financial discipline and keeps long-term financial planning realistic and calm. Small check-ins beat big overhauls.